It won’t surprise you that we have no software names in the portfolio. We spent the last week looking at the carnage on our screens, without really participating. For once, value stocks were not dragged into a broad market selloff and we have to admit, it feels kind of good.

We don’t have a strong view which pieces of software will or will not get disrupted by AI. In our simplified view on the world, most tech ends up getting disrupted by a few 20-year-olds in their mom’s basement, which is why we were always confused that those companies traded well over 30x P/E on average.

Figure: S&P500 Software Index TTM P/E (green) or Forward P/E (orange) which excludes SBC

We have repeatedly gone on record calling out the increasing stupidity in the market. We’ve had a ponzi (bitcoin) reach $2t in market cap. We’ve had a ponzi of ponzis (MSTR) argue for S&P500 inclusion as though they were a real business. We’ve seen the short squeeze in silver which Wallstreet has tried to re-engineer unsuccessfully since the 70’s. We’ve had a couple of nuclear and quantum science projects see their stocks go vertical.

We’ve done various articles on crypto and on bitcoin treasury companies. We called bitcoin the ultimate ‘greater fool’ asset, which would go up as long as there was a greater fool to step in every year. It looks like MSTR was the ultimate greater fool, one that will be difficult to top. The end result has always seemed inevitable. Our greatest surprise has been that the supply of greater fools seemed to be never ending.

We felt like old boomers seeing all our relatives and friends celebrate their crypto gains, while we steadfastly kept to investing in the real economy. Was this week finally the first factor rotation from ‘dumb stuff’ into real economy stocks?

Figure: Momentum stocks (red) underperforming this week vs value stocks (blue)

Talking about factor rotation into value feels a bit like being part of a religious cult that’s predicting the apocalypse. It’s easy to make bold predictions and it can get you a lot of followers, but for many decades the call for the apocalypse has been wrong to the point that if it ever happens, nobody will believe it even though it’s staring you right in the face.

Almost no company with real earnings and a reasonable valuation was down in the past week. We’re not talking about triple-adjusted, Non-GAAP emotional support earnings. We’re talking about real, boomer-era, GAAP earnings.

See, the greatest trick that management teams played on Wallstreet in the last decade, was the convince the market that stock-based compensation did not matter. Your Bloomberg terminal would show you P/E graphs based on forward looking estimates, which Wallstreet provided in line with how the management team wanted their earnings to look: excluding stock-based compensation (SBC).

Even the conservative, fundamental crowd started modelling SBC not as an expense, but as a percentage of dilution per year.

But that 4% dilution per year that they were modelling, just turned into 12% dilution now that the stock is down 70%. Does a company with no FCF and 12% dilution still deserve to trade at 10x revenue? Of course not! That’s how a stock down 70% ends up as a stock down 90%.

We love finding reflexivity in the market (and we’re not even talking about how Michael Saylor will fund his Perp dividends when MSTR trades below NAV). This is a classic case. A stock that’s going down in price while relying heavily on SBC to pay its employees will either be faced with unhappy employees, or endless dilution. Both would make the company worth less than when the share price traded at a higher level.

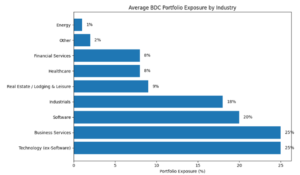

Will the selloff in dumb stuff cause contagion in any other sectors? The market certainly seems to worry about the impact on private credit, an industry on which we’ve also been outspoken bears. Various BDCs have become publicly listed recently, and it turns out that the public market doesn’t value those fee generating vehicles the same way the private markets have been marketing them for years. MSCI Income Fund (MSIF), Blue Own Capital Corp (OBDC) and FS Special Lending Fund (FSSL) are all trading roughly 20-25% below self-reported NAV.

And it’s not hard to see why the market is beginning to worry, given that software loans make up roughly 20-30% of the average BDC portfolio.

Source: Houlihan Lokey BDC Monitor, Fall 2025

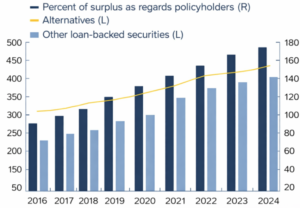

We’re watching the potential impact on the life insurance with great interest. Over the last few years, the lifers’ allocation to private credit has increased steadily. In fact, there have been some notable M&A deals where a lifer got acquired by PE with the explicit intention to create ‘permanent capital’ by investing more into their own private credit funds. Global Atlantic / KKR, Athene / Apollo, Allstate / Blackstone and Brighthouse / Aquarian come to mind. We expect to hear a lot more on this topic in the near future.

Figure: Life insurers changing investment portfolio. Source: S&P Global, Financial Stability Oversight Council

Meanwhile, with all the chaos in the market, we’d almost overlook January’s ISM PMI print. After 3 years of industrial contraction, we’ve got our first solid print above 50. One data point doesn’t make a trend, but we’ll be following this carefully in the next few months to see whether this will provide any support to real economy stocks.

Figure: ISM Manufacturing PMI. Source: Bloomberg, ISM

For now, we are enjoying the carnage from the sidelines, feeling thankful that real economy stocks have not gotten caught up in the selling pressure (yet). But we totally expect people to start selling their winners to buy the dip in the dumb stuff. We’ve got some cash to deploy once that happens!