Things may be light over the next couple weeks as we are in South Florida taking meetings during the annual iConnections pilgrimage. In our typical fashion, we don’t pay the 20k entry price to roam the halls, but rather sit with a cold beer at a local bar and laugh as the sleeveless vests descend upon the streets of South Beach jostling to meet Calpers to tell them how they have a differentiated strategy to buy NVDA…

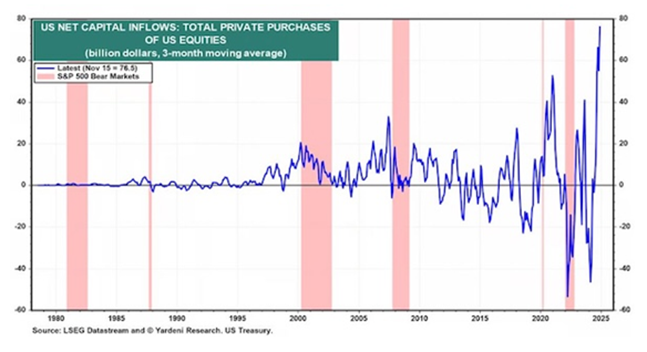

Nonetheless, our main thematics haven’t changed. Now that Trump is in, we expect a heavy dose of chaos and “sell the news” events to tick up. We already saw NVDA sell off hard on the back of Deepseek, even with the Stargate announcement and META ramping their capX. At some point, fund flows will flip and capital will drain from Mag7 and we’ll finally see mean reversion here:

The recipients of these flows will likely (hopefully) be their home countries as KEDM eyes more exposure in EM – Brazil, Turkey, and China. Speaking of the later, Trump hit Davos this week and spoke promisingly of Xi as sentiment perks up there. Meanwhile, Xi unveiled more plans to bolster their stock market as the CSRC greenlit insurers to invest 30% of new premium into A shares (upwards of $100B Yuan) and want Companies to continue to ramp buybacks and divvies. Could the Year of the Snake may finally be the year of the bull??

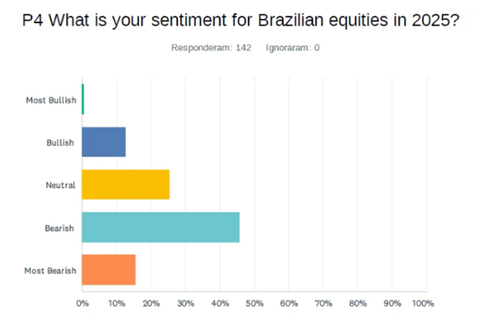

And over to Brazil, we encourage you all to read through our good friend (and previous Happy Hour guest), PauloMacro’s Brazil post this week. He is our local expert there and has been bearish for 15 years, but recently flipped bull. Even if we get the timing off by a bit, EWZ is yielding 9% for a market trading at 8x forwards. With the US elections now behind us, our eyes now move over to Brazil’s 2026 election for the catalyst. With sentiment this bad, it won’t take much…