Theme of the Week

Kliff Note of the Week

Spin-off Monitor: Baidu (BIDU)’s spin-off of its AI chip unit, Kunlunxin, is progressing well. Some sell-side reports estimate that Kunlunxin could be worth $16-23bn standalone, and considering Baidu’s 59% interest, the spin-off could unlock ~$10bn (against a $42bn market cap).

BIDU used to derive most of its revenue from online marketplaces, but nowadays the AI Cloud business accounts for almost half of its revenue. And while a bit weird to mention, its robo-taxi operations are actually doing quite well.

BIDU recently announced a $5bn share repurchase program and a first-ever dividend policy. It might be worth keeping an eye out.

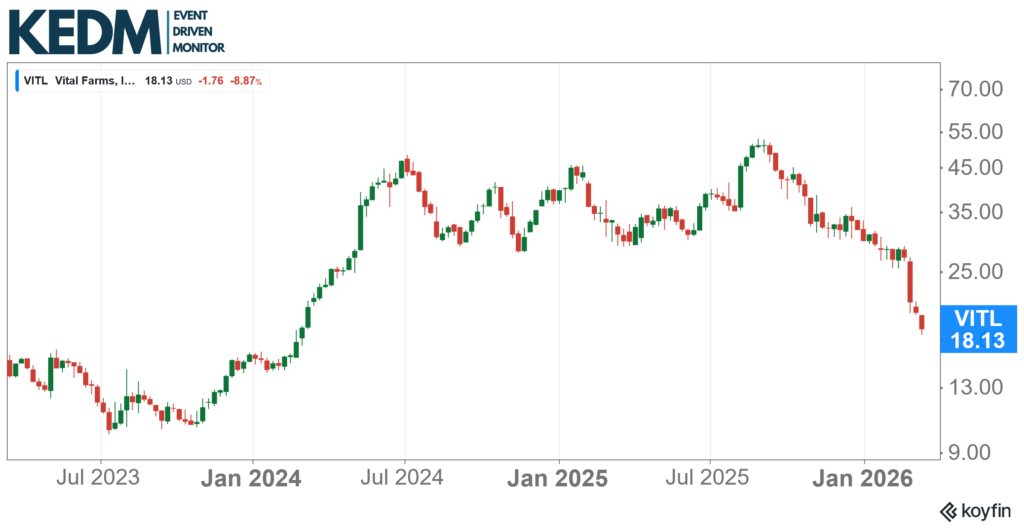

Announced Buyback Monitor: Vital Farms (VITL) popped up on the screens after announcing a $100m buyback, roughly 10% of its market cap. There are several things we don’t like here, such as slowing growth, the founder/ex-CEO steadily selling shares, the share count creeping up, and an ugly price momentum.

But we still added VITL to the watchlist as there’s also plenty to like. While slowing, organic growth remains very healthy, with plenty of operating leverage left; healthy FCF generation, which should only improve as the base matures; ‘healthy and ethical farming’ is a nice secular trend; decent valuation at <7x forward EV/EBITDA. It might be too early, but we’re watching this one.

CEO Turnover Monitor: Chemicals company Syensqo’s (SYENS BB) new CEO has barely started, and the company is already out with a huuuge profit warning. While the first reaction might be ‘new CEO kitchen sinking’, the warning was all based on stuff that was already going on, but it all just got much worse.

Despite the share price action, this still looks like a decent short. If your largest segment is called Specialty Polymers, and that division is massively under pressure and showing no signs of being ‘special’ at all, that’s an issue.

Also, the 2026 guidance already seems too high. And the company is still trading at ~8x forward EV/EBITDA; AKE FP and EVK GY are trading at 5-6x. In short (no pun intended), we wouldn’t be surprised to see it trade down to those levels.

13D Monitor: Pearson (PSON LN) is not yet in full activist mode but is getting there. Cevian is at 18% and Artisan at 10%. The stock is down big time on AI‑disruption fears, despite a multi‑year shift toward AI‑enabled education tools.

Artisan says the market is mispricing Pearson as an AI loser and is ‘open’ on a potential US listing. Cevian has previously pushed for exactly that. There is a good chance this one will be taken out, in our view.

Strategic Alternatives Monitor: We flagged waste management company Enviri (NVRI) a few weeks ago. Enviri is selling its Clean Earth business, and we can expect large capital returns and what looks like a rather cheap remainco.

NVRI’s recent Q4 print was a mixed bag but still supports the asymmetric setup. The Environmental segment (the piece that matters for Remainco) is holding up well, with 2026 EBITDA guided comfortably above 2025. Total 2026 EBITDA guidance of $140m is also ahead.

But a bit softer part was management backing away from confidence in the $14.50-16.50 p/s cash payout landing near the top end, citing some uncertainty around how much cash they’ll need to retain.

That said, this is still a rather large payout (on a ~$18 share price) with plenty of rerating potential left on the Environmental unit alone.

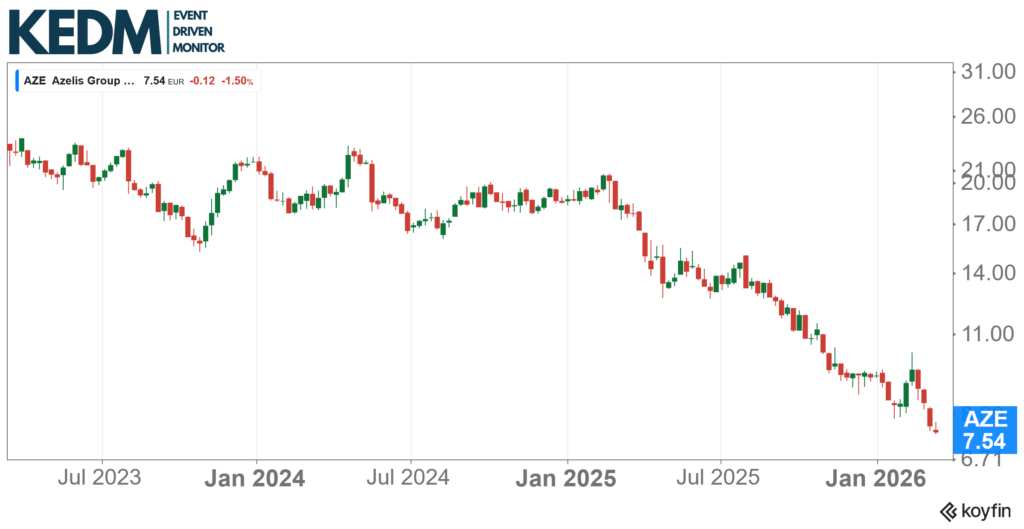

Other Interesting ED Action: EQT sold its last stake (~10%) in specialty chemicals distributor Azelis (AZE BB), finally completing its exit. The share overhang has often been mentioned as a major reason for the large discount to IMCD (roughly 30%).

With the sale, two of the three reasons often cited for a discount are gone; the overhang is cleared, and communication has improved (read: the CFO has been replaced).

The third reason is lower liquidity vs IMCD, but that gap is slowly closing. IMCD has a longer track record, but for the rest, these two companies are the same, and there shouldn’t be a large valuation discrepancy.

KEDM Event Driven Monitor scans over 20 corporate events for market moving information and distills them into our propietary “Kliff Notes.” One profitable trade should more than cover an annual subscription and access to the Event Driven chatroom!