Let’s start with our recent big announcement.

We’ve been quietly levelling up KEDM these past few months — sharper themes, improved Kliff Notes, a better format, and stronger content overall.

But something was still missing. The small and mid-cap space, full of overlooked opportunities, needed its own dedicated product.

That’s why we recently introduced KEDM Lite, our newest addition to the KEDM family.

It’s a curated feed of potentially actionable setups, built from the same Pro dataset that powers our main monitors.

Each weekly issue of Lite delivers:

- 30+ actionable special situations and event-driven ideas (42–46 issues per year)

- Deeper focus on small and mid-caps, where alpha often hides

- Happy Hour webinars with our own Kuppy and guests, plus AMA sessions

- Full Lite archive access, growing into thousands of highlights over time

Check it out with a free trial, which also gets you access to the upcoming

Which brings us to our next big event: Happy Hour

This Friday after the close we are back with another Happy Hour.

Grab a 6-pack and join Kuppy as he sits down with Freddy Brick, partner at Muddy Waters. Freddy joined Muddy back in 2014, right in the thick of one of the most interesting stretches in the short-selling business, and before that, came from APAC activist powerhouse, Oasis.

Translation: he has stories from the trenches. A lot of them. On top of that, Freddy has spent years investing across Asia and has recently launched both a mining fund and a Vietnam fund, giving him a fresh lens on today’s biggest opportunities.

A quick reminder: A free KEDM Lite trial also gives you access to the Happy Hour!

Theme of the Week

IPOs

The last three years in equity markets have felt straight out of the roaring 60s. However, despite the strong performance of US indices, the U.S. IPO market has been oddly lukewarm over the same period. US and European IPO volumes are well below 2021 levels, with only Hong Kong making a big rebound in 2025.

The 2026 IPO slate is no exception. We’ve been explicit about the limited profit potential for most AI names, yet here we are talking about record IPO valuations. After 3 years in which the stock only went up, we are seeing all the usual signs of a market where making money has been too easy.

So why do we track IPOs? Because the chance of mispricing is very large for a new security. Prices are set by flows, not by fundamentals. Pension funds are still waiting for their favorite banker to tell them what the shares are worth. In hot stocks, animal spirits are taking over, driving stocks to irrational levels. When there is a mispricing in the market, there is an opportunity.

Kliff Note of the Week

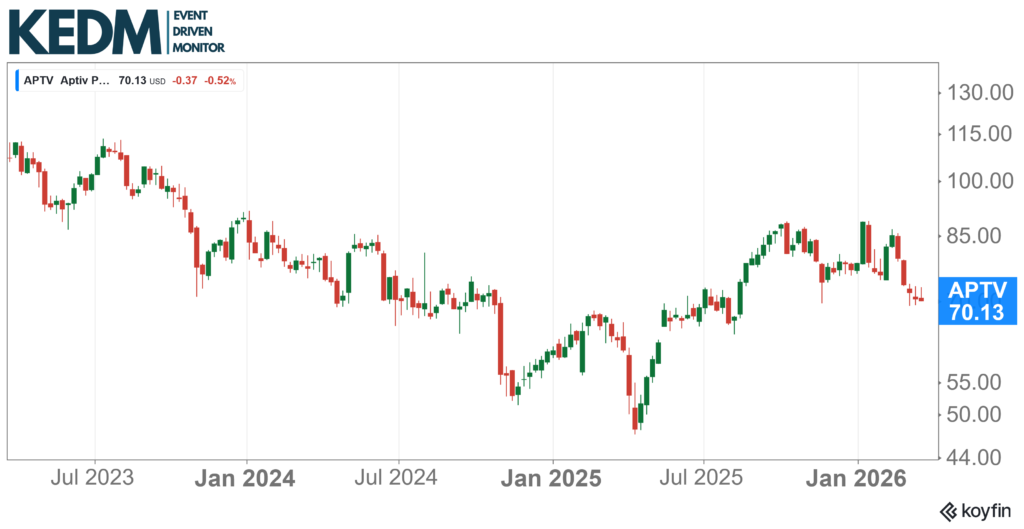

Spin-off Monitor: Aptiv PLC (APTV) spin-off is progressing. The record was announced as Mar 17: one SpinCo. share for every three APTV shares. To elaborate on the situation, APTV is spinning off its lower-margin Electrical Distribution Systems (EDS) business and retaining its higher-margin software business.

For 2024, EDS business had $8.3bn in revenue with 9.5% EBITDA margin, whilst the software business had $12.2bn in revenue with 18.8% EBITDA margin. The SpinCo will raise a total of ~$2.1bn in cash via senior notes and a credit facility, of which at least $1.7bn will be paid back to the Parent company as a special dividend.

Upon completion of the transaction, RemainCo will have a cleaner balance sheet and the potential for a re-rating to higher multiples. At the same time, SpinCo will be a leveraged pure-play wiring harness and electrical distribution business for OEMs.

Usually, with spin-offs structured this way, SpinCo faces selling pressure upon trading, creating a potential value gap. The SpinCo will be named Versigent and traded on the NYSE under “VGNT” from Apr 1.

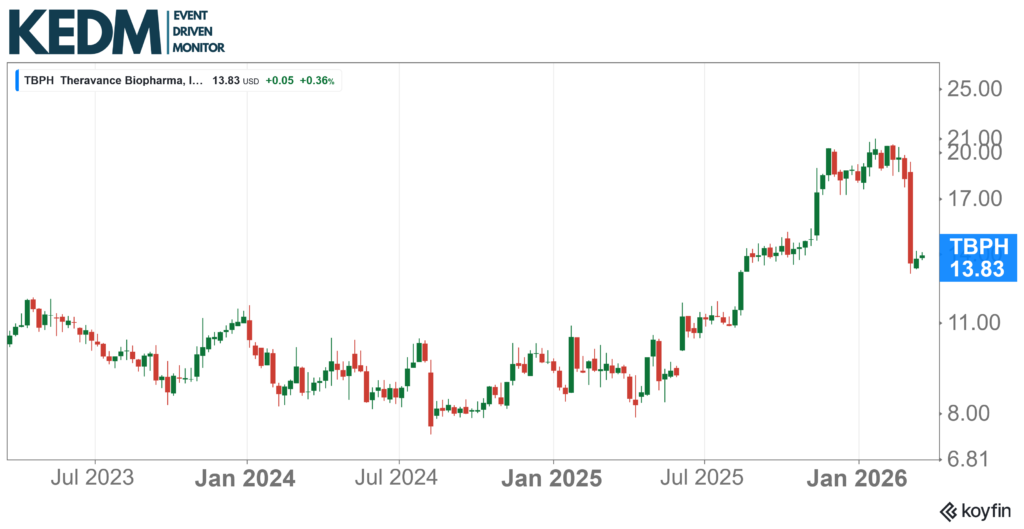

Strategic Alternatives Monitor: We’re generally wary of flagging biotechs, because who the heck knows. Certainly not us. That said, here’s an interesting biotech. Theravance Biopharma (TBPH) shares recently dropped almost 30% on the failure of its Phase 3 CYPRESS study.

While clearly disappointing, this might create an opportunity with more visibility. The company is now accelerating its strategic review and cutting costs aggressively, shrinking its operations to focus on Yupelri, a growing COPD asset with a long patent life.

The cost savings and growing products will push the company to generate $60-70m cash flow per annum. They expect to have a $400m net cash position by Q1, with an additional $100m from Trelegy-related milestones.

So, in short, $500m net cash and an asset generating $60-70m in cash flow, on a $690m market cap. Worth a look.

Investor Day Monitor: Marex (MRX) will organize an investor day on March 26th, 2026. This is already their second investor day since their IPO 2 years ago, and we doubt they have a new story to tell.

We think management believes they are misunderstood by the market, with earnings being much less volatile than the market tends to expect. Their recently reported Q4 was a record quarter despite being a seasonally weak one (the holiday season), but now the market is back to fearing interest rate sensitivity.

In the call, they said the high vol in the market isn’t quite Goldilocks, but they are well underway to grow in line with long-term ambitions, which, if true, would put 2026 EPS at $5.

Newsletter Shorts Monitor: Hunterbrook updated its initial short-side report for RadNet, Inc (RDNT). The original thesis was that the company is trading at over 2x the premium of its peers because of its AI branding, even though AI-related revenue is less than 5%, and same-center growth was misleading. In this week’s update, Hunterbrook stated that it removed the same-center metric from its 10-K, which arguably validates the initial claim.

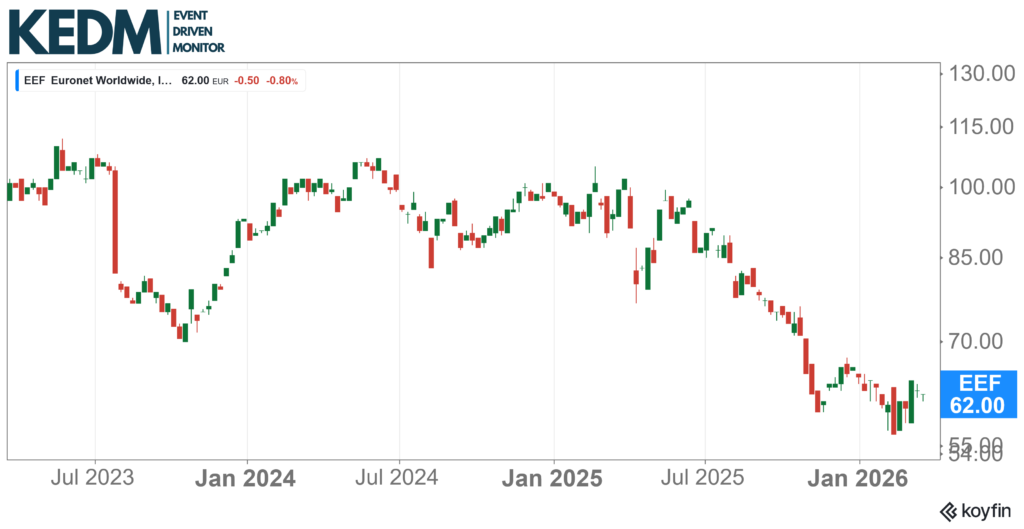

13D Monitor: Voss Capital has been increasing its position in Euronet Worldwide (EEFT) and sending angry letters, pushing the company to review strategic alternatives.

Despite almost all fundamentals moving in the right direction, Euronet’s share price had a horrible 2025, mostly on (fears of) increasing competition from digital-first rivals such as Wise and Remitly.

Voss argues that parts like payment processing and money transfer could be valued more highly on their own. A full sale could deliver even more (100%+ potential), as it will also monetize Euronet’s global licenses and cash generation.

Also, it is worth noting that Euronet has been (and continues to be) a true share cannibal.

M&A Monitor: Multiple bids for Reservoir Media (RSVR), now up over 30% since we flagged it a few weeks ago (always look at our Other Interesting ED Action section!).

We already had Irenic Cap offering $10-11 p/s (a range indeed). Now Wesbild, together with Richmond Hill, is offering $10.50 p/s in cash. Wesbild already owns 44%, and Irenic has over 9%.

What makes this all the more juicy is that CEO Golnar Khosrowshahi’s father controls Wesbild. Golnar is also the cousin of Dara Khosrowshahi, Uber’s CEO. We would argue there’s a pretty good chance that this one will be taken out.

Still 5.5% spread on Webild’s offer, and we could even see a bit more to entice Irenic to sell its stake.

KEDM Event Driven Monitor scans over 20 corporate events for market moving information and distills them into our propietary “Kliff Notes.” One profitable trade should more than cover an annual subscription and access to the Event Driven chatroom!