Theme of the Week

Reflections on the Energy Trade

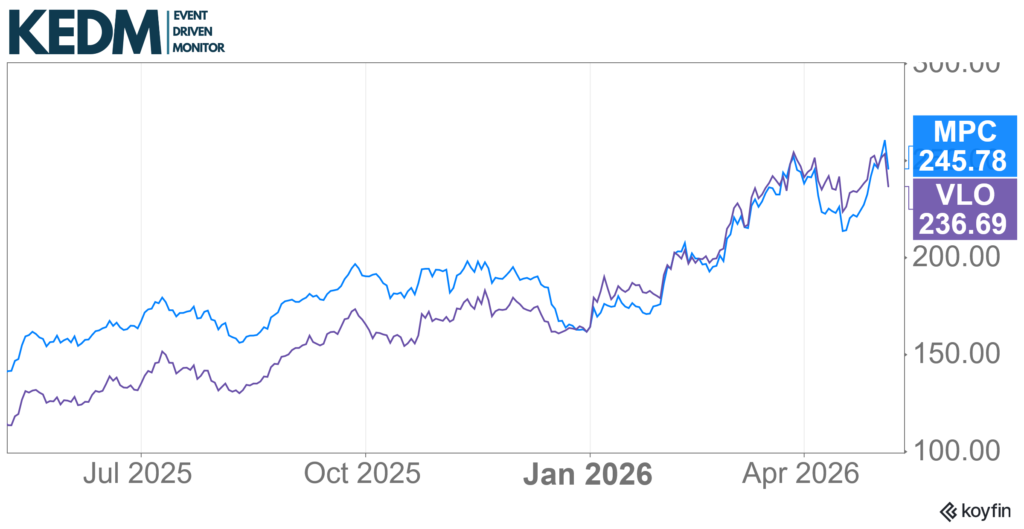

As we’d described in our September 2025 (Vol # 241) write-up on refiners, we are now expressing our view on oil & gas through refiners. Demand for refining capacity tracks oil consumption, which means it grows roughly 1-2m bbl per year.

But supply growth should be constrained in the second half of this decade. Meanwhile, most refiners trade at a fraction of replacement cost.

The US large-cap plays (VLO, MPC) on this theme have performed well since the write-up.

The Iran war really put fuel on the fire with crack spreads now well over $50. Refiners are printing money in this climate.

High jet fuel prices, as well as feedstock advantages for US refiners – which can access cheaper heavy crude from Canada or Venezuela, has made this investment many times more profitable than even we had expected less than a year ago.

Kuppy’s Tweet of the Week

We recently introduced KEDM Lite, our newest addition to the KEDM family.

Each weekly issue of Lite delivers:

- 30+ actionable special situations and event-driven ideas (42–46 issues per year)

- Deeper focus on small and mid-caps, where alpha often hides

- Happy Hour webinars with our own Kuppy and guests, plus AMA sessions

- Full Lite archive access, growing into thousands of highlights over time

*Early subscribers to the annual plan will get access to the KEDM Discord room. All

Kliff Note of the Week

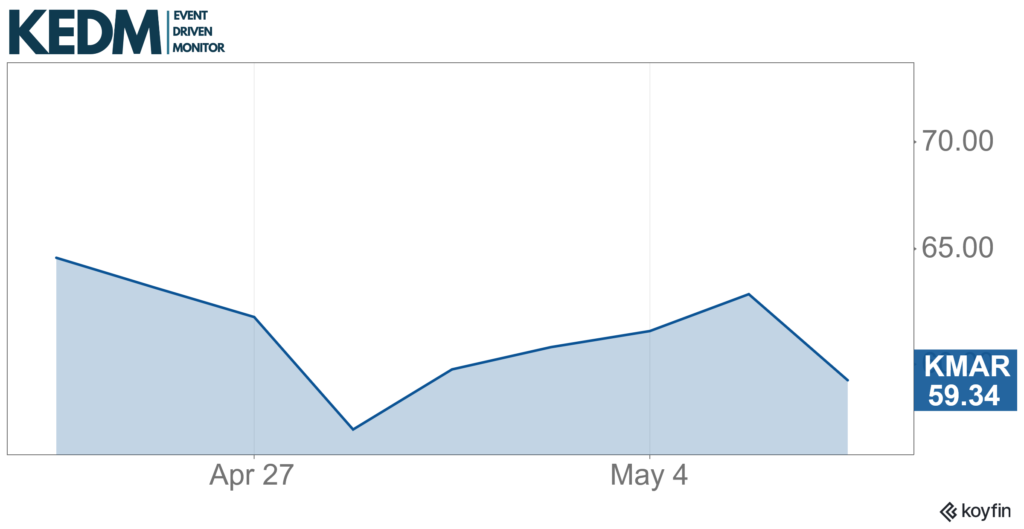

Spin Monitor: The Kongsberg Maritime (KMAR NO) spin was completed on April 23. Kongsberg also recently held a capital markets day. Another interesting company exposed to European electrification and defense tailwinds.

Solid growth, margins, and order backlog so far, and KMAR is targeting further improvements. Worth taking a look.

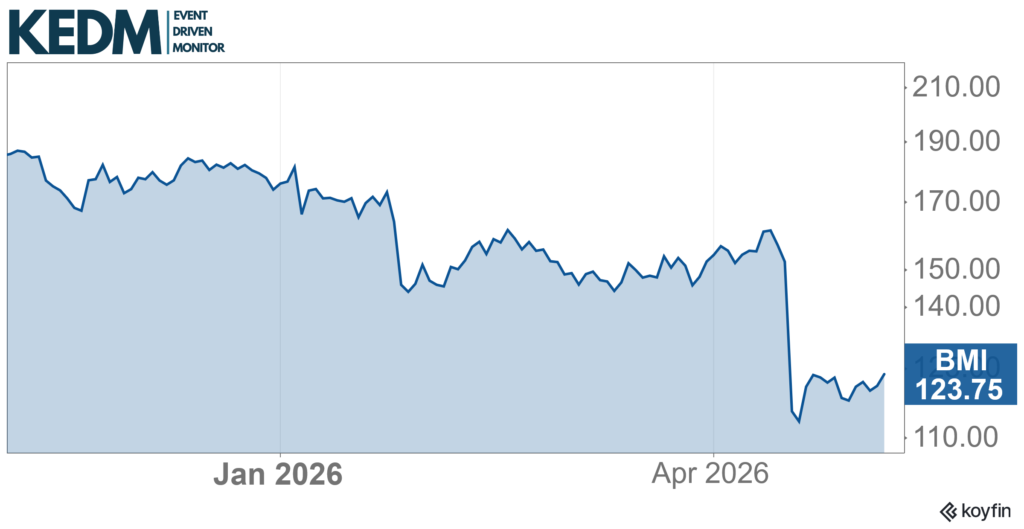

Investor Day Monitor: Flow control company Badger Meter (BMI) is not having a good time, with the shares down more than 50% over the past year.

The last hit was on weak results, but these were mainly due to two non‑structural issues: the (rather normal) project‑pacing gap between completed AMI deployments and not‑yet‑started awards, and an unexpected $15-20m short‑cycle slowdown.

Despite slowish growth, gross margins are holding up well, and costs are under control. Insiders have been buying the dip, and BMI will hold its first investor day in over 7 years in May. We suspect a very bullish story.

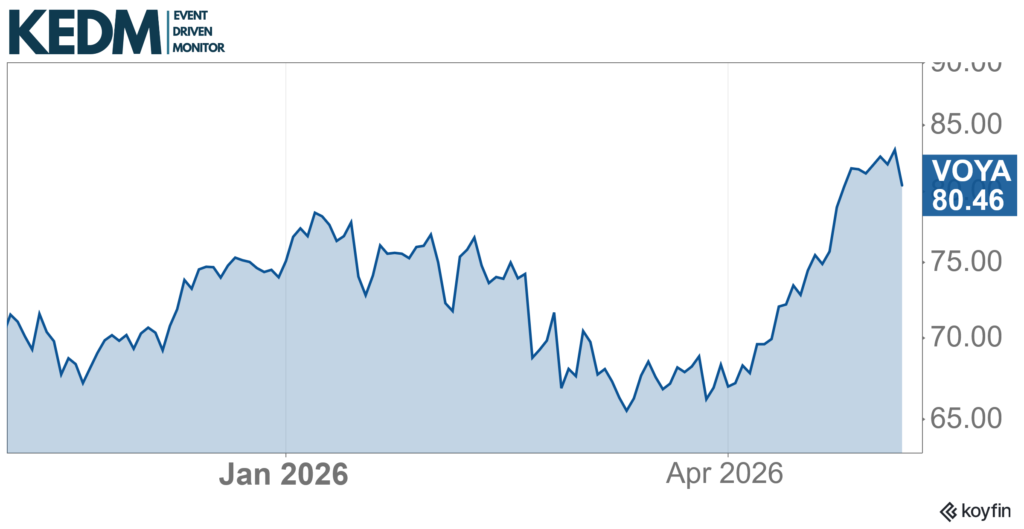

Activist Monitor: Activist TOMS Capital took a stake in Voya Financial (VOYA) and is pushing the insurer to pursue strategic alternatives, that is, either a full sale or divestment of its underperforming health‑benefits unit.

That business posted a $10m pretax loss in Q4 and materially lags group margins. Meanwhile, the group is posting double-digit operating margins and trading at ~8x forward PE.

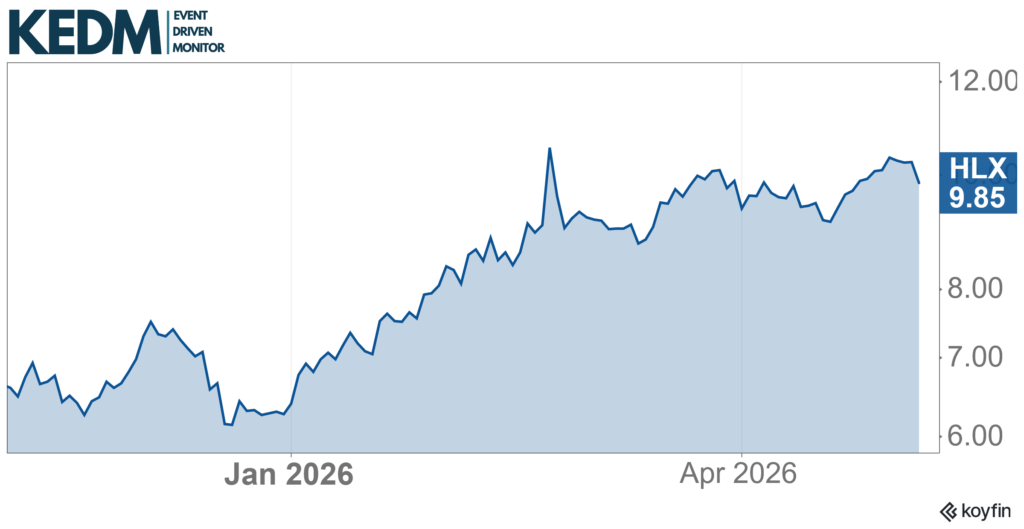

M&A Monitor: Hornbeck is returning to the public market, not by selling out to Tidewater (TDW), but by merging with Helix Energy (HLX) to combine HOS’s MPSV and OSV fleets with HLX’s subsea business.

Expected close in H2, after which this will trade under the ticker HOS. 6x 2025 EV / EBITDA by our math, with $75m of synergies promised (14% of EBITDA) and 21 vessels still stacked and 2 MPSVs to be delivered in 2027.

We’ve been told that the stacked vessels in the bayou have trees growing out of them, so buyer beware.

Strategic Alternatives Monitor: Aspo (ASPO FH) is a Finnish conglomerate that has been reviewing strategic alternatives, with the recent sale of one of its three divisions (Leipurin) for a total cash consideration of €62m.

The remaining two businesses (ESL Shipping and Telko) are also still being assessed. A glance at these units suggests their values, as reflected in Aspo’s current enterprise value, are pretty conservative.

A quick SOTP guesstimate puts us at €550- 600m enterprise value, implying 60-100% potential upside on the equity. It might be worth doing some work on it.

Other Interesting ED Action: Just flagging this VersaBank (VBNK) deep dive from our friends at Crossroads Cap.

VBNK is a digital bank trading at roughly book value despite two major growth engines: strong upcoming US expansion and the Real Bank Tokenized Deposits optionality.

There’s a good return potential on a successful US expansion, but truly multi-bagger potential should their RBTD strategy pay out.