Theme of the Week

Trading the Chaos

We wrote about the market’s unrealistic expectations regarding how easy it would be to reopen the Strait of Hormuz. For decades, the market has speculated about a worst-case scenario: Iran closing the Strait of Hormuz.

Yet when it finally happened, we found ourselves numb to geopolitical risk, confident that Trump’s tolerance for bear markets would eventually lead him to TACO.

Look, it is now the entire world’s (ex-Russia and Iran) #1 priority to get the oil flowing again. Humans are inventive, and they tend to figure things out if they try hard enough.

And Trump believes this conflict can end whenever he chooses, meanwhile filling the supply gap with an SPR release.

We are open to the idea that this could be resolved one way or another. But we’re waiting for clarity in the market, and we leave it to others to buy the dip, assuming that once Trump TACOs, everything will revert to normal.

In July of last year, we wrote that Trump’s presidency would surely increase volatility. We argued that commodity brokers were a perfect way to benefit from all this volatility.

We nailed the volatility call. January’s -30% silver selloff (20-sigma!) was soon eclipsed when Brent shot up 30% in a day, only to end lower. Higher trading volumes accompany all this volatility.

Kuppy’s Tweet of the Week

We recently introduced KEDM Lite, our newest addition to the KEDM family.

Each weekly issue of Lite delivers:

- 30+ actionable special situations and event-driven ideas (42–46 issues per year)

- Deeper focus on small and mid-caps, where alpha often hides

- Happy Hour webinars with our own Kuppy and guests, plus AMA sessions

- Full Lite archive access, growing into thousands of highlights over time

*Early subscribers to the annual plan will get access to the KEDM Discord room. All

Kliff Note of the Week

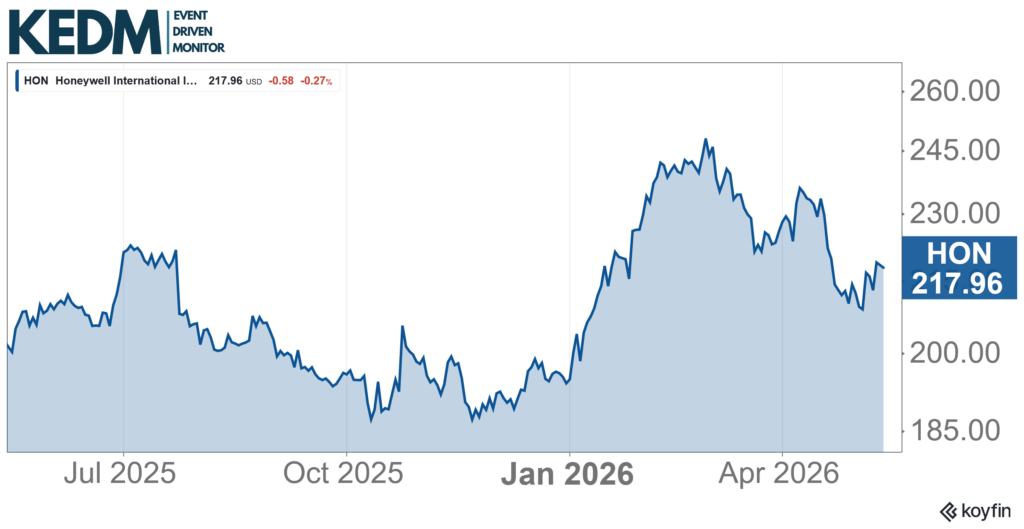

Spin Monitor: The Honeywell Aerospace (HONA) spin is expected to be completed on June 29. Honeywell Aerospace will hold a capital markets day on June 3 to discuss strategy and guidance.

Aerospace faced a tough Q1 on supply chain disruptions, ending a long streak of quarters with solid growth, though March was solid again.

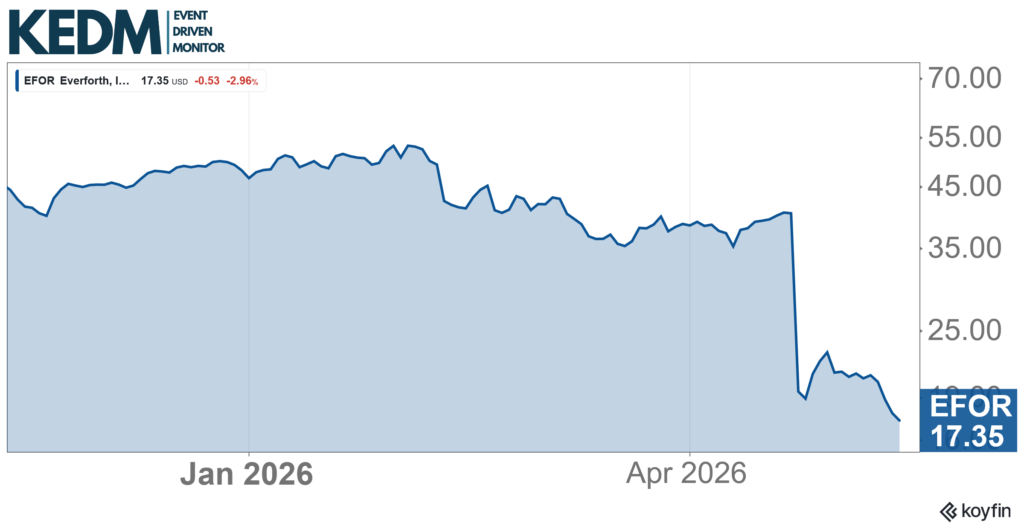

Cluster Insider Buy Monitor: Everforth (EFOR), the recently rebranded ECS, has seen insiders strongly buy the dip, putting up almost $2m. And this was a big dip, with shares dropping almost 50% on very poor earnings and a guidance drop.

Everforth has been working to rekindle growth after experiencing topline pressure for some years now. Still solid FCF generation. ~6x forward EV/EBITDA. EFOR still has room for >$900m in buybacks.

Newsletter Shorts Monitor: It’s full-on damage control at Sportsradar Group (SRAD). Earnings miss, estimate, and target price cuts across the board, and oh, short reports (e.g., Muddy Waters) claiming that Sportradar generates a meaningful portion of revenue from illegal operations.

The company is countering with a $1bn buyback (~30% of the market cap), o/w $250m accelerated.

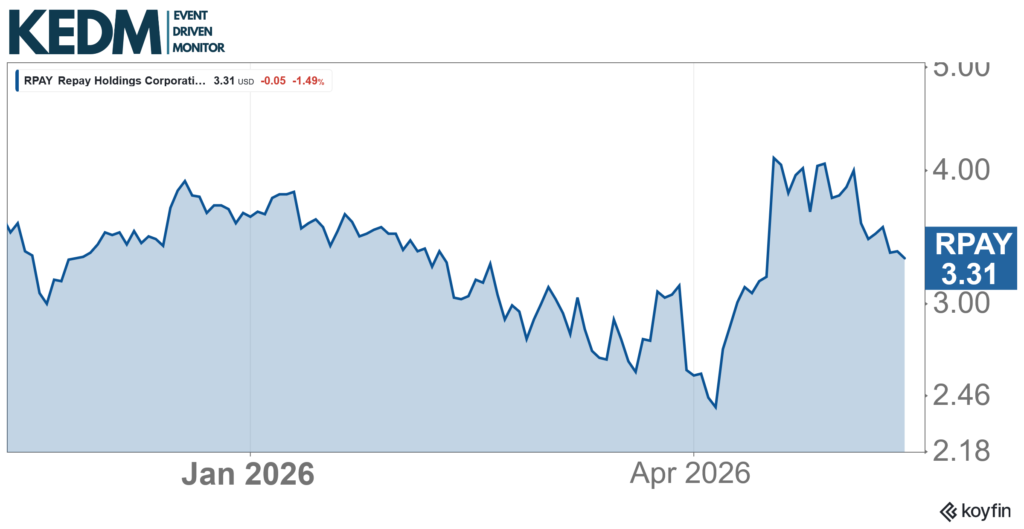

13D Monitor: Forager is losing patience with Repay (RPAY) and is criticizing the board for failing to engage ten days after receiving Forager’s proposal. As a reminder, Forager is offering $4.80 p/s in cash to take RPAY out (vs c. $4.10 today).

RPAY holds ~13% and is buying strongly before submitting the offer. Despite the decent premium on the recent share price, the offer would just bring the company back to where it was a few months ago.

Meanwhile, #2 holder Veradace continues to add. Expect more action.

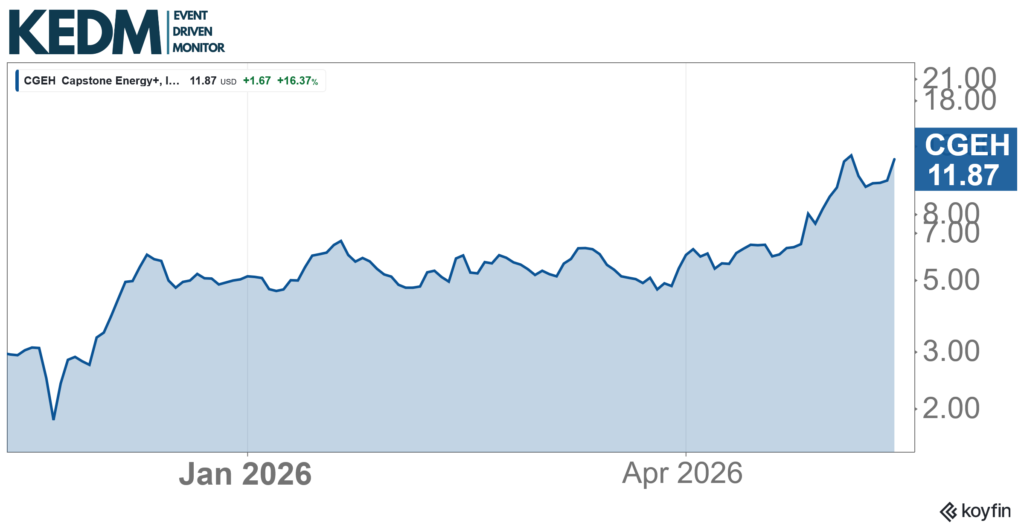

Listing Changes Monitor: We’ve recently flagged old out-of-bankruptcy play Capstone Green Energy (CGEH) as (in our view) still very strong risk/reward, despite the shares of the microturbine power company having done extremely well.

Good execution, revenues growing by over 20% in the recent quarter, solid margin development, 14-17x EV/EBITDA. But this is all before any data center-related revenues, which are in the pipeline and are a massive opportunity.

How massive? Well, just take a look at what big brother Bloom Energy (BE) is doing. The shares are up over 10x in a year, yet they still cannot keep pace with the massive revenue and earnings growth.

What a beast. And this is all hidden CGEH potential. Still trading OTC; uplist to Nasdaq on track for H2.

Strategic Alternatives Monitor: We’ve started to do some work on Ziff Davis (ZD). Ziff popped up on our insider buys screen in September of last year.

Much of Ziff consisted of legacy assets with little growth, yet the company still had attractive margins and decent cash generation. More recently, they sold their Connectivity division for $1.2bn cash, ~60% of the current enterprise value. Not bad for 16% of revenues (though a larger part of operating income).

But there’s plenty of assets left (e.g., Health & Wellness, Gaming, etc.); we won’t be surprised to see continued clean-up, shareholder returns, and a potential rerating of its core digital assets.