Theme of the Week

Special Purpose Acquisition Corps (free tutorial)

As part of our tutorial series, we wanted to dive into our SPAC monitors and explain why, despite their track record as value destroyers, we continue to track SPAC deals. Many of our subscribers know all there is to know about SPACs.

If that’s you, we advise you to scroll through this section quickly, have a glance at the data showing how disastrous SPAC returns have really been, giggle at the memes (hopefully), and then go straight to the event-driven section. After our Easter break, there is a ton to share on the ED side.

We recently discussed the poor performance of IPOs. We saw the average pop 19% on the day of the IPO, only to underperform by 20% over the next 3 years.

The money is made by whoever gets an allocation in a hot IPO, which, at the end of the day, is just a return on all the commissions you’d paid your investment banker in the prior year.

But you cannot discuss SPACs without discussing Chamath Palihapitiya, the king of blank-check companies, who at one point raised money under the tickers IPOA, IPOB, all the way to IPOF…. (download the full free tutorial below).

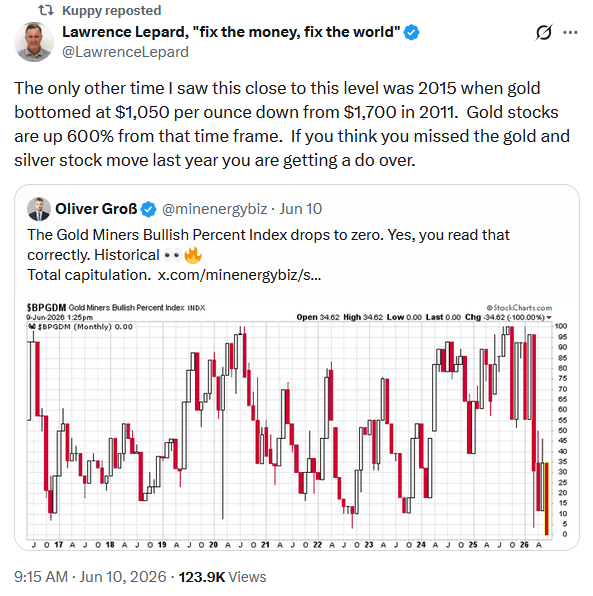

Kuppy’s Tweet of the Week

Want to just cut through the noise and get actionable event-driven ideas?

KEDM Lite is a must for event-driven investors.

Each weekly issue of Lite delivers:

- 30+ actionable special situations and event-driven ideas (42–46 issues per year)

- Deeper focus on small and mid-caps, where alpha often hides

- Happy Hour webinars with our own Kuppy and guests, plus AMA sessions

- Full Lite archive access, growing into thousands of highlights over time

*Early subscribers to the annual plan will get access to the KEDM Discord room. All KEDM Pro subscribers get Lite for free!

Kliff Note of the Week

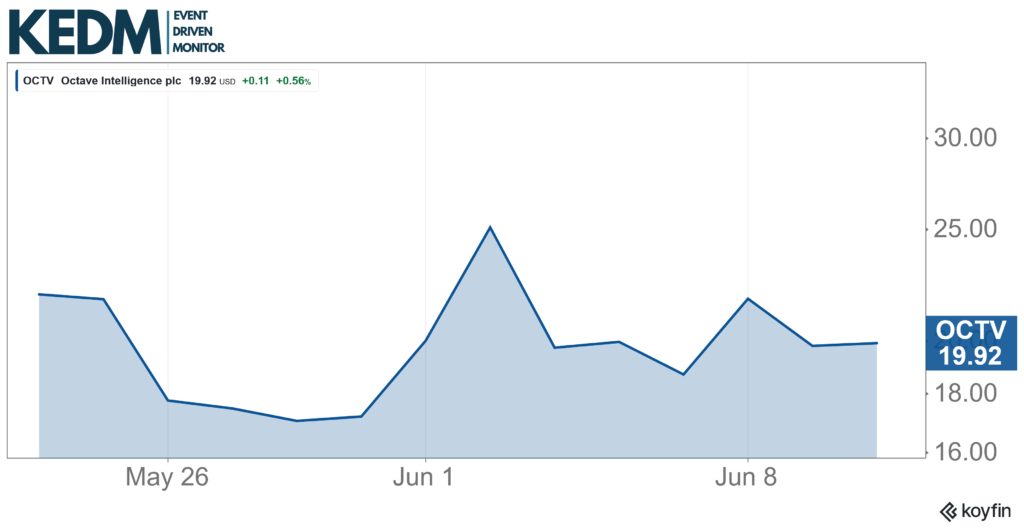

Spin Monitor: Hexagon (HEXAB SS) completed the spin of Octave Intelligence (OCTV), and the shares are down >20%. It’s software, so that might make sense.

Octave intends to restore growth and profitability, with medium‑term guidance for >10% ARR growth (up from hsd), ~30% operating margins (stable) and 23-24% FCF margins (from 20%).

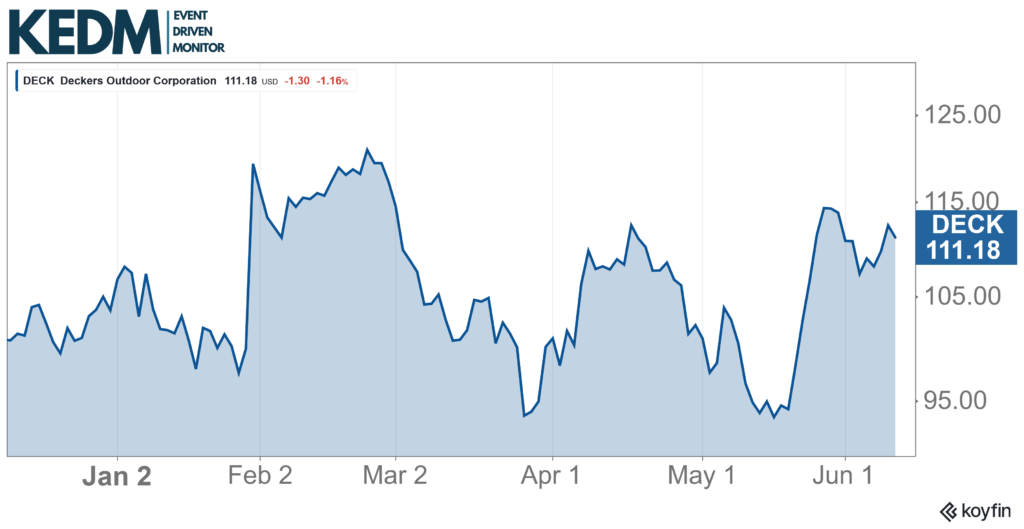

Buyback Monitor: Deckers Outdoor (DECK) recently increased its buyback authorization by $3.5bn to $5bn. Not bad for a ~$15bn market cap.

And it makes sense: msd-hsd topline growth, >20% EBITDA margins, over 70% FCF conversion, strong and rapidly increasing net cash position. They bought back ~6.5% of s/o last year. 10x EV/EBITDA seems too low.

13D Monitor: Jana (~5%) is pressuring Alkami Technology (ALKT) to restart the sales process. Alkami already explored options earlier this year, but no deal was concluded.

Alkami is another fintech software company that has been crushed by AI disruption fears. Interestingly, insider buying activity has picked up strongly in recent months, with #1 shareholder General Atlantic also very active, now at roughly 18.2%.

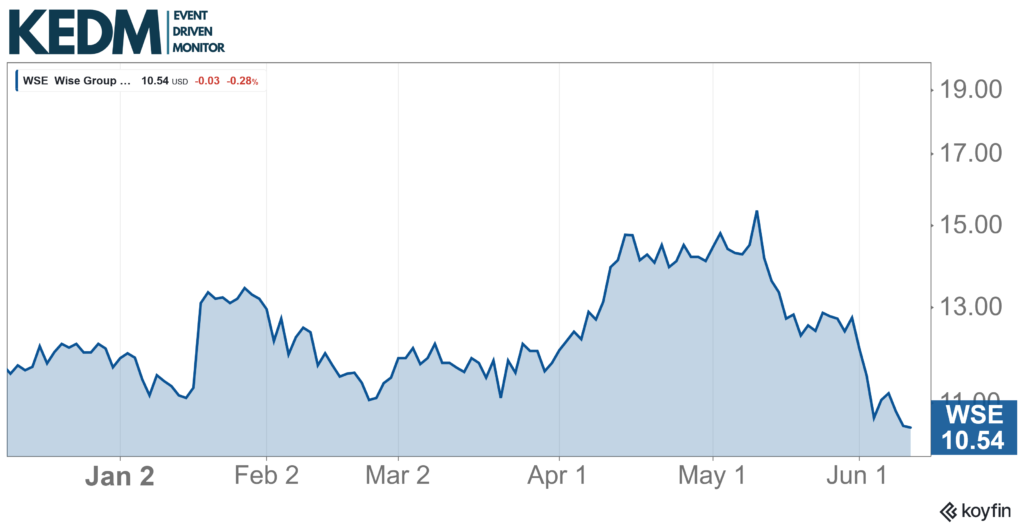

Other Interesting ED Action: Wise (WSE) is under pressure after Belgian prosecutors disclosed an investigation into anti‑money‑laundering failures, claiming that hundreds of customers moved ~€500m in suspicious funds through the platform.

The probe has been active since late 2025 and is now in an ‘advanced stage’, and checks whether Wise accounts were used for fraud, corruption, and drug‑trafficking, and, of course, whether the company performed adequate due‑diligence checks.

Who knows what the fines will be, but as far as we can remember, the highest we’ve seen in similar cases was ~$2bn (HSBC and Danske). So this looks quite priced in, right?

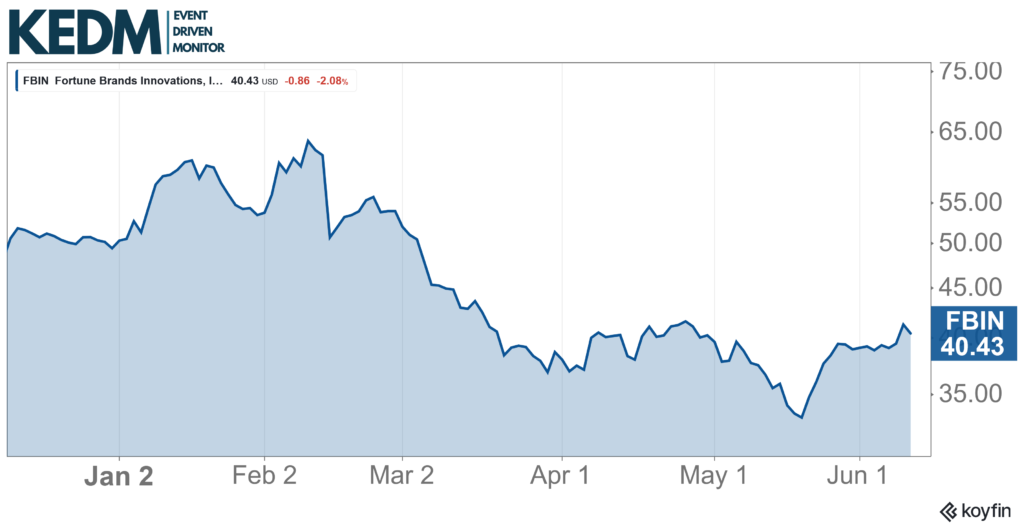

Strategic Alternatives Monitor: Fortune Brands Innovations (FBIN) launched a strategic review of its composite‑decking unit Fiberon, shifting toward its higher‑margin, less capital‑intensive Water and Security businesses.

While we don’t expect much value creation from the sale, the fact that FBIN is willing to sell assets, combined with a new incoming CEO, might finally lead to some healthy strategic decisions (i.e., more large asset divestments).

Other Interesting ED Action: Team Internet (TIG LN)’s CEO recently said in an interview that the company has received multiple competing bids for the DIS unit and suggested that the implied valuation should be >$180m, enough to retire all debt and return cash to shareholders.

That would leave TIG trading at roughly 70% net cash, with the remaining, now-infecting, rest of the business (Comparison and Search) valued at only ~2x EBITDA.

Also, the Search division should be booked as held for sale, with TIG already in discussions (as per their November PR).