This week, Transocean (RIG) announced their intended acquisition of Valaris (VAL), thereby further consolidating the offshore drilling space. At KEDM, we have been involved in offshore energy since both Noble (NE) and VAL emerged from bankruptcy in 2021. With clean balance sheets and a slowly recovering energy market, we believed both companies were well positioned to benefit massively if offshore energy were to eventually recover from their decade long bear market.

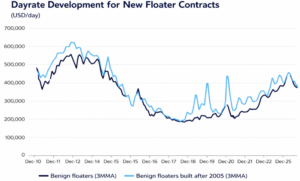

In the 3 years that followed UDW day rates recovered from roughly $200k to $505k, which was still well short from the $681k booked by the Transocean Deepwater Pathfinder in 2013.

Mid 2024, we were all caught off guard when a shortage of FPSOs further down in the energy value chain formed a bottleneck. The industry hit a pause and tender activity came to a halt. Rigs had to get sent back to the Canary Islands to get warm-stacked, while some outdated semi-submersibles went straight to the scrap yard.

We exited our position during 2025 and while we picked the bottom and offshore perfectly our exit could have been timed a little better.

Our concern was that the 2024/25 pause in offshore activity would extend until 2026 (it did) or maybe even 2027 (it might). Furthermore, low utilization rates tend to go hand in hand with lower day rates (day rates fell to $380k). VAL was looking at having 7 out of 13 offshore rigs being off contract by the end of 2025 and would have to get more aggressive on pricing. RIG had been disciplined in putting all their rigs to work, in part forced by their high leverage, while VAL failed to understand that they are a price taker, not a price setter.

Modern 7g or 8g rigs also continue to become more efficient, with drilling speeds having tripled since the last cycle. Could we see a situation where we need a lower number of rigs to do all the work, similar to the permanent drop in US onshore rig count?

With day rates down into the high $300k, and oil floating around $70, we are genuinely surprised to see offshore having performed as well as it has.

Figure: Day Rates (USD / day) over the last 15 years. There has been a noticeable step down since the peak in late 2024.

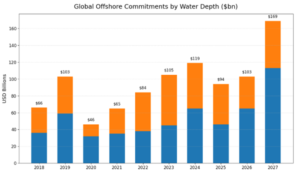

Industry insiders still expect global Offshore spending to recover in 2027. However, this spending is still pending an FID and any project slippage would move this further into the future.

Figure: Tidewater’s projections of offshore spending

Reflecting on the acquisition by Transocean, it’s a win-win-win. Valaris shareholders get to cash a quick premium of roughly 31%, paid in RIG shares. RIG gets to deleverage their balance sheet, cut back some redundant overhead and show their shareholders accretion on EV / rig. RIG has a track record of doing acquisition funded with shares, which are effectively hidden capital raises (remember Ocean Rig?).

Meanwhile a less leveraged RIG can be less aggressive while bidding on new work, and they can now potentially retire some of their 6th-generation rigs, which should benefit the entire industry.

This brings us to today, where the major drillers are all trading at low-double-digit FCF multiples. That’s quite rich for companies with depreciating assets and a cost of debt of >8%. It is still cheap on steel value, especially in relation to today’s replacement cost, but there is at least some recovery priced in. We think the long term trend remains intact, but we’ve moved on to other trades.

As we’d described in our September 2025 (Vol # 241) writeup on refiners, we are now expressing our view on oil & gas through refiners. Demand for refining capacity tracks the demand of oil consumption, which means it grows roughly 1-2m bbl per year. But supply growth should be constrained in the second half of this decade. Meanwhile most refiners trade at a fraction of replacement cost.

The US large cap plays (VLO, MPC) on this theme have performed well since the writeup.

Figure: VLO and MPC stock performance since the KEDM writeup on refiners

Crack spreads have been volatile, but the overall direction is up. They have benefited from the fact that Russian refineries are not drone-proof (see the spike in November) as well as strong diesel demand from Europe.

Figure: Nymex WTI Cushing Crude Oil 2:1:1 crack spread (CRK211M Index), Source: Bloomberg

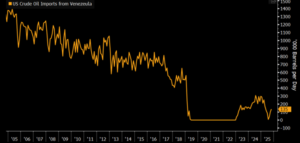

A potential return of Venezuelan crude further benefits the high Nelson complexity US refineries on the Gulf Coast, who are well equipped to handle the much cheaper Venezuelan crude. The real benefit happens when Venezuela increases their crude production, which is probably a few years out. But S&P Global reports that US refiners are already processing low hundreds of kbpd, while they historically processed 500-800 kbpd. Venezuelan crude can easily add a few dollars to the crack spread.

Figure: US crude oil imports from Venezuela Source: Bloomberg

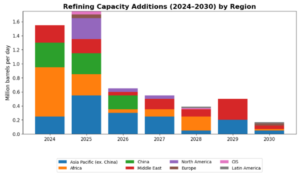

But with all the cyclical reasons impacting crack spreads, it’s easy to lose sight of the longer-term trend, which is that new supply of refining capacity is falling off a cliff starting this year. And as we explained earlier, this supply forecast includes refineries in Nigeria (Dangote) and Mexico (Dos Bocas) that are unlikely to reach nameplate capacity.

Source: BloombergNEF, company announcements

We fully expect crack spreads to remain volatile in the short term. Peace between Ukraine and Russia, or at least a halt to Ukraine’s drone attacks on Russian facilities, would be bearish. And an end to Russian sanctions would bring could bring another 400k bbl/d of refining capacity back, which is now offline because of the difficulty Russia faces in maintaining their refineries, without access to the required spare parts.

We’re here for the long-term trend, and we would welcome any short-term dip.