Special Purpose Acquisition Corps

As part of our tutorial series, we wanted to dive into our SPAC monitors and explain why, despite their track record as value destroyers, we continue to track SPAC deals. Many of our subscribers know all there is to know about SPACs. If that’s you, we advise you to scroll through this section quickly, have a glance at the data showing how disastrous SPAC returns have really been, giggle at the memes (hopefully), and then go straight to the event-driven section. After our Easter break, there is a ton to share on the ED side.

We recently discussed the poor performance of IPOs. We saw the average pop 19% on the day of the IPO, only to underperform by 20% over the next 3 years. The money is made by whoever gets an allocation in a hot IPO, which, at the end of the day, is just a return on all the commissions you’d paid your investment banker in the prior year.

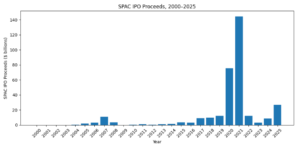

Given that KEDM was launched in 2020, it won’t surprise you that we’ve been tracking SPACs (Special Purpose Acquisition Corps) since our inception. SPACs were hot in 2020 and 2021. In those 2 years combined, more than $200b was raised in the form of blank checks, with the promise to use this for future acquisitions. For most of the investors, this has ended in tears.

Source: Initial Public Offerings: Updated Statistics Jay R. Ritter 2025

With the bull market in dumb stuff, which gained steam in 2025, we are not surprised to see this financial structure making a comeback, as we’ve learned from studying the Weimar Republic: under Project Zimbabwe, people like to gamble their rapidly depreciating fiat. At the end of the day, SPACs allow them to do just that.

A SPAC, in its essence, is a group of promoters who convince the market that they are really good at acquiring companies. They go to the market to raise money, promising that the funds will be used to acquire a yet-to-be-determined company. Units in this shell company are generally priced at $10. In addition, investors often receive warrants priced at $11.50 to give them the illusion of free upside, even though they effectively issue those warrants to themselves.

The cash is put in a trust account where it earns the risk-free rate. Meanwhile, the sponsors look for a deal and then put it up for a vote with SPAC investors.

This means SPAC investors buy free optionality. If they don’t like the deal, they can vote against it and get their money back, including interest. In this case, they will have earned the risk-free rate, while the sponsor will have borne all the costs of sourcing a deal. In fact, if you vote against the deal but enough other investors vote in favor so the deal goes through, you get your money back while keeping your warrant.

That’s the simplified bull thesis for SPACs. Until the day the acquisition goes through, it’s a risk-free cash shell with free optionality.

The problem is that on the day the SPAC completes, you lose the downside protection provided by the cash trust. After all, the cash gets spent on the acquisition.

And it’s clear from the above that the SPAC sponsors have every incentive to sell their investors on the proposed deal. If the deal gets rejected, they will have spent millions of their own money on due diligence, with nothing to show for it. If the deal gets approved, they end up with a significant ownership in the new entity. 20% as a promoter fee is quite typical.

Not surprisingly, most SPACs end up acquiring easy-to-promote story stocks: space travel, blockchain, fintech, rather than a business with good fundamentals.

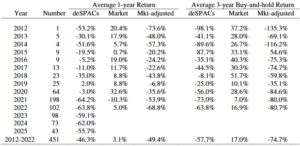

Over 1 year, the average SPAC underperformed the market by 49.4%. On a 3-year basis, underperformance ended up at 74.7%.

Source: Initial Public Offerings: Updated Statistics Jay R. Ritter 2025

The track record is made worse by the fact that most SPACs occurred in 2020-2021, a period when the IPO/SPAC window was wide open. Many companies that lacked the foundation needed to be a public company (think internal controls, ERP systems, profitability, or, in many cases, even revenue) went to market prematurely. In fact, many companies going public had no shot at becoming successful businesses. Yet, they still managed to raise money by promising space travel, flying cars, or anything related to fintech or green energy.

But you cannot discuss SPACs without discussing Chamath Palihapitiya, the king of blank-check companies, who at one point raised money under the tickers IPOA, IPOB, all the way to IPOF. He didn’t just have his name on 6 different SPACs. His presence could turn the promise of space travel into billions of dollars of committed capital. 5 years later, 3 out of his 7 ventures have cost his investors meaningful money, while 2 SPACs failed to close. The last one, SOFI, is still ‘in the money’, although activist short seller Muddy Waters thinks that won’t last long either.

In Chamath’s defense, he was in the arena trying stuff.

For the promoters, SPACs were a simple way to trade their dignity and reputation for staggering amounts of promoter fees.

You’d think this track record would make it impossible to raise money again. However, memories on Wall Street are short. In late 2025, Chamath raised $300m for America Exceptionalism Acquisition Corp (AEXA). In contrast to the previous structures, this SPAC comes without warrants, and the promoter shares are performance-linked: they will only pay off if the post-merger stock rises to $15. This is guaranteed to result in even more stock promotion. And if it doesn’t work, there will be no crying in the casino.

Figure: Chamath is not taking anyone’s advice

Successful SPACs are rare. DraftKings (DKNG), SoFi Technologies (SOFI), and Vertiv (VRT) are among the few that have benefited from a tailwind and are still trading above their $10 IPO prices.

For now, we are still tracking SPACs. As mentioned, the free optionality a SPAC provides is valuable if that option has a high chance of closing in the money. In a market where empty promises and dreams can be well received (read: many SPACs can trade well above the $10 NAV), holding pre-deal SPACs instead of cash can be a decent strategy.

Maybe the market gets one last hit of SPAC opium before reality smacks this structure down. Sure, we like a gamble, but even a casino offers better odds than holding a post-merger SPAC. Then we can quietly retire the SPAC monitor and chase something that actually makes alpha.