It increasingly looks like Trump convinced himself that killing the top hundred guys in Iran would somehow fix Iran. It did not.

So now we appear to be moving to plan B: the classic Washington strategy of bombing things until they resemble a parking lot.

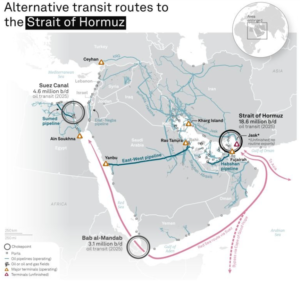

There is just one small issue. Iran’s best negotiating chip is the Strait of Hormuz, through which roughly a fifth of the world’s oil flows. If that closes, the entire global economy suddenly remembers where energy actually comes from.

And closing it is not particularly complicated. The Houthis managed to make shipping in the Red Sea miserable for almost two years with far fewer resources. You don’t need a strong naval force to bring trade through the Strait of Hormuz to a complete halt. This is something 2 bros on a boat with an RPG can take care of.

Now imagine the same thing but with far bigger consequences. When the Suez Canal was closed, container vessels could go around the Cape of Good Hope. Sure, it was a detour, which added to costs and made the Europeans wait a little longer for their Temu order, but at least there was an alternative. In the case of the Strait of Hormuz, there is only one way out.

Figure: There is only 1 way out. Source: S&P Global Energy

There is also a second problem with the decapitation strike. If you eliminate the entire leadership of a country, you also eliminate the people you would normally negotiate with when things start getting messy.

Even in World War II, the Allies were careful not to vaporize every senior Nazi. You needed someone left who could pick up the phone and tell the remaining fanatics that the war was, in fact, over.

Japan had the same issue. The emperor surrendered and some soldiers still kept fighting on remote islands for years because no one could convince them otherwise. It is in everyone’s interest that Iran has some sort of leadership.

But who is exactly in charge of Iran right now? And more importantly, who is in charge of the guys with missiles who are currently extremely angry. The nightmare scenario is not a coordinated Iranian state response. Fragmentation can be far worse.

Picture a handful of generals turned regional warlords, each with enough hardware to disrupt shipping, each with a financial incentive to keep the Strait of Hormuz closed while extracting payments from anyone desperate enough to move oil.

People talk about naval escorts solving this. Talk to anyone who actually works in shipping. Escorting tankers through a narrow choke point while everyone has drones, mines, and anti-ship missiles is hardly a solution. Trump can provide government backed insurance for oil tankers all he wants, but there is the issue that most captains and their crew are not willing to die for the sole purpose of saving the global economy. Nobody likes the idea of sailing a giant tank with 100 thousand liters of highly flammable fuel through a combat zone.

And the U.S. is not sending ground troops to reopen the strait. What is the strait remains closed enough for somebody else to step in? Imagine Saudi Arabia deciding that controlling the choke point is easier than coordinating production quotas through OPEC.

Over the last year, the market had grown numb to geopolitical risk, with most wars being over before Globex futures started trading on Sunday evening. Think February 2020 and COVID-19. For weeks nobody cared. Then it became the only thing anyone cared about.

Oil is similar. A few dollars higher does not matter. Markets can absorb that. But if roughly twenty million barrels per day of liquids moving through the Strait of Hormuz suddenly become uncertain for even a few weeks, that stops being a price move and starts being a systemic problem.

Sometimes the correct trade is simply to de-gross, keep your powder dry, and wait to see which direction the chaos breaks.

Now let’s talk about trading it.

The first thing you are seeing is the usual market reflex. Oil spikes and everyone immediately starts screaming about inflation again. Cue the talking heads explaining how the Fed is now trapped forever.

Yes, higher oil feeds into inflation. That part is obvious. What is less obvious is that if global shipping freezes, credit markets do not exactly function smoothly either. And when credit markets freeze, central banks suddenly rediscover their inner dove.

Picture oil at some absurd level while private credit stops moving for a couple of weeks. Suddenly, the debate shifts from higher for longer to please cut before something breaks.

That’s why we’re eyeing SOFR futures. If credit locks up, rates get repriced quickly. High oil prices do not automatically imply a tighter policy. Sometimes it forces the opposite.

Tail hedges are awkward right now. It is too late to buy disaster protection cheaply, but also too early to assume nothing happens. The simplest play is boring but effective: cut gross, raise cash, and grab the cheapest disaster insurance you can find.

For some, that means calls on the VIX. Not perfect, but volatility tends to spike when chaos hits. Think of it as the cheapest condom in the pharmacy. Hopefully it never gets used.

Fortunately, Europe has had 4 years to work on its energy security since the last military shock that forced it towards cold showers and virtually ended the German industrial complex.

Unfortunately for Europe, they seem not to have gotten that lesson. Even though Europe seemed to be slowly getting out of its inflation-induced downturn of 2020-2022, with wage growth finally exceeding inflation, that recovery goes back in the drawer now that the attention shifts to how to get people a hot shower.

There are very few bull markets left in Europe. Military spending is one that is surprisingly selling off in line with European equity markets.