When KEDM was launched back in 2020, one of the most popular sections was the Fallen Angel monitor. This monitor flagged a handful of companies that had fallen completely out of favor and whose shares traded at inexplicably low prices.

As the saying goes: You can make a lot of money when something goes from hopelessly fucked to somewhat shitty.

In hindsight, 2020 and 2021 were the perfect year to make money with this monitor. The world had gone on lockdown and many businesses who were deemed non-essential were forced to close. Without customers or employees showing up for work, most businesses were hopelessly fucked, and they had the share price to show for it.

But then it became clear that most of us were going to be just fine, and the plebs was packed with their Covid stimmies and was slowly allowed to tread outdoors again. All you had to do to make money was ignore the short-term noise and take a long-term view. And when many companies saw the environment move to only somewhat shitty, and in some cases even fantastic, most names on this list printed money.

Over time. the Fallen Angels slowly lost their place in KEDM as we decided to focus more on big thematics as well event driven trades. In hindsight, that timing worked out well. The last few years have gotten increasingly difficult for anyone who’s had the misfortune the care about valuation. A stock that’s down 90% can easily go down another 50% and hurt your quarterly performance.

The market seems to have evolved into a combination of factors. Goldman Sachs will gladly sell you a basket of ‘AI Losers’ to short, or ‘End-of-year tax losers’ to buy. The wisdom seems to be that a company with negative earnings momentum can be shorted regardless of valuation because you can just hedge the valuation factor by owning something else that’s cheap. Your valuation factor goes to 0.

Remember those stocks you own that missed earnings by 1% yet sold off 30%? Last quarter seemed to be particularly bad for those names. Stocks can go down 20% because the market anticipates they will miss earnings, another 20% when they miss earnings, and another 10% when sell-side confirms that they have indeed missed earnings.

We’re not a single stock newsletter and we do not intend to be. But at the same time, we scan so many names across our various screens, and we continuously call out underappreciated companies. It would be a shame not to track some of the real outliers in their special monitor. We’re also seeing increasing evidence that being able to take the ‘long’ view does occasionally pay off, at least once you’re past the vicious cycle of earnings revisions.

For that reason, we’ve decided to bring back the Fallen Angels monitor.

Our intention is not to flag trashy companies with a bleak future. Our interest is in businesses seeing some sort of positive earnings inflection. Some of the companies we follow are just too niche to warrant their own thematic writeup.

But don’t worry, we’re not suddenly bottom fishing in (still) overvalued SaaS names with excessive SBC. Some stocks go down for good reason.

Over the next few weeks, we’ll slowly start populating this monitor with names we’re tracking. Keep in mind, valuation no longer provides a floor to stocks. If your company is in the crosshairs of a pod shop who’s decided that you own an AI loser, there is no limit to how low your shares can go. We totally expect some of those names to go down further. As always, they’re not recommendations.

At the end of the day, we strive to be your best source for idea generation. KEDM is the publication you give to your analyst on Monday morning, telling him to work out the ideas that best fit your style by lunch.

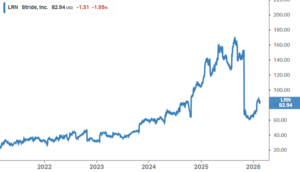

Stride (LRN)

LRN is part of a duopoly with Pearson that operates virtual public schools. Customers are charter schools and school districts who pay LRN per student. Covid showed people that home schooling is an option and even in 2026, demand is still growing. There have been short reports since 2013 alleging ghost students. What matters is, demand is real.

After Q1 results, the shares crashed from $160 to ~$60 because they announced problems with the integration of a new software system, which had slowed enrollment. At Q2, they announced those problems were under control, but 2026 will be a no growth year. At no growth, this capital light business is arguably too cheap at 7x EBIT or 9.5x FCF. If it returns to 10-15% growth next year, why wouldn’t it trade at its historic 15x EBIT?

Janus International (JBI)

JBI is a near monopoly (80% market share among the public storage REITs) on doors for self-storage. Doors are 5% of the total cost of self-storage, but they are mission critical. A well-functioning door means you can operate the facility with no employees.

This is indirectly a play on a recovery in existing home sales (a favorite KEDM theme). There is a commercial business (think: doors for truck warehouses) which recently disappointed (blamed on project timing), leading to the selloff. Management has a murky history of setting guidance. Beware, JBI has not yet shown it has ‘bottomed’, but this is ~10x FCF (at hopefully trough margins) and if commercial’s setback was indeed just a timing issue, this should quickly rerate.

Icon Group (ICLR)

Rightly or wrongly, Clinical Research Organizations (CROs) have been labeled as AI losers and are down ~25% YTD. Running clinical trials is a labor-intensive business that will probably see some efficiencies from AI. Industry growth used to be 3-4% growth in pharma R&D funding, with an additional 3-4% from outsourcing. Will increased outsourcing offset most of the AI related efficiencies?

As we flagged last in last week’s KEDM, ICLR sold off an additional 40% when they postponed their Q4 reporting to April, and said they’d likely restate revenues downward by ~2%. Revenue recognition under their ‘percentage of completion method’ is complicated and the most probable cause of the restatement. There is no indication that the $1b in annual FCF isn’t real, which makes the company cheap at 7x FCF.