Last week, we wrote about how the market’s unrealistic expectations of how easy it would be to reopen the Strait of Hormuz. For decades, the market has speculated about a worst-case scenario: Iran closing the Strait of Hormuz. Yet when it finally happened, we found ourselves numb to geopolitical risk, confident that Trump’s tolerance for bear markets would eventually lead him to TACO.

Look, it is now the entire world’s (ex-Russia and Iran) #1 priority to get the oil flowing again. Humans are inventive, and they tend to figure things out if they try hard enough. And Trump believes this conflict can end whenever he chooses, meanwhile filling the supply gap with an SPR release. We are open to the idea that this could be resolved one way or another. But we’re waiting for clarity in the market, and we leave it to others to buy the dip, assuming that once Trump TACOs, everything will revert to normal.

But we are students of history, and we don’t even have to look that far back to see how difficult it was to gain control of the Suez Canal when the Houthis decided to close it. Many multi-year wars began as short-term military interventions.

It’s only been 2 weeks, and we must all be getting tired of everyone’s geopolitical take. We do not mean to pile on. Instead, we want to focus this week on what this means for some of the KEDM thematics, and we just leave the current situation to the following:

As we discussed last week (including in our Discord room, where we give more frequent updates), our initial response was to de-gross and get rid of everything we don’t feel comfortable adding to on a dip. We bought some quick-tail hedges while we waited to get more clarity on how the situation would unfold. We cleaned out our event-driven book, given those positions, opting instead to hold only the names we know well. But we held on to our positions that, at least in theory, benefit from the current chaos.

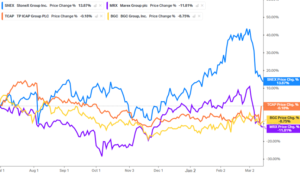

Long Vol Basket

In July of last year, we wrote that Trump’s presidency would surely increase volatility. We argued that commodity brokers were a perfect way to benefit from all this volatility. We nailed the volatility call. January’s -30% silver selloff (20-sigma!) was soon eclipsed when Brent shot up 30% in a day, only to end lower. Higher trading volumes accompany all this volatility.

Both BGC (BGC) and TP ICAP (TCAP LN) commented on their recent earnings call on how they are benefiting from the current environment. Stonex (SNEX) and Marex (MRX) just reported record quarters in Q4, mainly driven by high volumes and wide spreads in metals trading (as well as a very interesting structural growth angle in MRX’s prime brokerage business).

But how wrong were we to think the market would care about earnings growth? Admittedly, both SNEX and MRX commented that the recent levels of vol are “too high to be considered goldilocks”. While exchange volumes are clearly up (+12% on CME in Jan and Feb, although much higher in metals and energy), the higher margin requirements drain liquidity and reduce trading activity. Hedging activity is shortened or postponed altogether, as nobody wants to lock in high prices they think are temporary. That doesn’t mean it’s negative. Both companies are simply managing expectations and emphasizing that earnings are less volatile than the market tends to think.

MRX is still guiding to a 10-20% structural growth trend in Profit Before Tax, which, if true, would put the company at 7-8x 2026 P/E. Their PE sponsors still have one 17% tranche to sell, which probably won’t happen until after Q1. That will be the cleanup print.

SNEX closed on the acquisition of RJ O’Brien, effectively turning the middle market into a 3-player oligopoly: if you’re a BSD moving billions, you get to deal with JPM or GS, but for everybody else, your options are SNEX, MRX, and ADM. We love consolidating markets with growing demand.

The market seems concerned about credit risk if its clients can’t meet margin calls. Historically, the largest non-fraud-related losses occurred during COVID, when oil prices fell into negative territory. ABN Amro clearing lost ~$200m, with IBKR losing around $100m. Those were exceptions. There is a slightly longer list of instances where an FCM lost $10-40m on a trade gone wrong. If that’s the worst-case scenario for both SNEX and MRX, it would amount to a bad quarter. But most importantly, MRX and SNEX would point to their risk management track record, and neither company pointed out any relevant losses when they updated the market only a week ago.

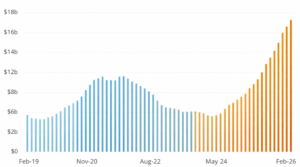

Mineral Drilling

We last updated on mineral drilling in December 2025. We argued that higher gold and silver prices and renewed investor interest would enable miners to raise more capital.

This bull market is just starting. Recent capital raises haven’t yet boosted drilling revenues for companies like Major Drilling (MDI CN), but they will. Despite the lack of profit growth, MDI has run up a fair bit in anticipation of an uptick in activity. Once junior miners get access to capital, you can be sure that it will be deployed in exploration, so they can show the market how promising their drilling rights are, if only they could get a little more funding.

Since our last update, junior miners have continued to raise capital. We are happy holding on to a theme that benefits from more chaos.

Figure: Trailing Twelve Month Equity Raises for junior miners, Source: Bloomberg

Refiners

We spoke about our bullish view on refiners in September of last year, based on our belief that we’re headed into a supply-demand mismatch. We updated this recently after a potential ramp in Venezuelan heavy oil production, which was supportive of US Gulf crack spreads due to lower transportation costs and a discount on heavy crude oil, which US refiners with high Nelson complexity are designed to handle.

Despite the recent risk-off environment, refiners have been resilient. Middle distillate (jet fuel, diesel) is up, partially offset by higher oil prices. US refiners enjoy another edge: they run on natural gas, which remains plentiful domestically.

We will keep an eye on how this unfolds. There is roughly 16m bbl of crude coming out of the Persian Gulf, and another 6m bbl of products. Let’s assume 5m bbl of crude will still find its way out either through Yanbu or Fujarah. That is still a supply/demand mismatch of 5m bbl for global refining capacity (excluding the Persian Gulf). Some positives and some negative forces, with uncertainty about which will prevail.

Tankers

We haven’t been involved in tankers of this size since the IMO2020 trade and the Covid oil contango, but in situations like today, they can be a great way to express a view.

Both clean and dirty rates are up. With the Arab Gulf out of the supply picture, distances stretch, and rates spike. Eventually, if the market dries up, there won’t be enough oil to ship, and rates will collapse.

Figure: Baltic Dirty Tanker Index. Source: Bloomberg

As for clean tankers, beware of countries implementing export restrictions on oil products. One day, when all this is over, every country will need to replenish inventories, and arbitrages will open up, probably driving much higher clean tanker rates. But we think we’ll get export restrictions first.

If you do own tankers, make sure they’re not trapped in the Persian Gulf, and if they are, make sure they are earning demurrage.

Figure: Baltic Dirty Tanker Index. Source: BloombergFigure: Baltic Clean Tanker Index. Source: Bloomberg

But most importantly, stay liquid. The best way to play events will become more apparent over time. Don’t deploy your dry powder too early. Good luck! Now over to our events.